2017-2020 China New Energy Vehicle and Vehicle Battery Development Forecast

True lithium research predicts that China's new energy vehicle sales will reach 454,000 vehicles in 2016, an increase of 27.57% year-on-year. In the next few years, it will increase at a rate of 2 to 3 percentage points per year. By 2020, the growth rate will reach 36.75. %, by then, the total annual sales volume of new energy vehicles will be around 1.44 million units. In conjunction with the four ministries and commissions in October 2015 (NDRC, National Energy Administration, Ministry of Industry and Information Technology, Ministry of Housing and Urban-Rural Development), the " Electric Vehicle Charging Infrastructure Development Guide 2015-2020" The forecast target given in the report is equivalent; the total possession is about 4.8 million vehicles, which is slightly different from that target, but it still performs best on a global scale.

Figure 8. Forecast of production and sales of new energy vehicles in China from 2016 to 2020 (unit: vehicle)

Overall, the True Lithium study believes that the Chinese government is still able to achieve its minimum target of 5 million. This is because China's political system determines that the government's policy formulation is quite flexible. Once it is found to be wrong, it will adjust at any time. In the context of increasing experience in recent years, the attitude of policy adjustment will become more and more rational.

Possible adjustment measures are as follows: 1 In the case that the downward trend of battery cost is greatly slowed down, the extent of subsidy decline may also be moderately slowed down; 2 if the annual sales volume of electric passenger vehicles is significantly different from expectations, the subsidy policy is also Will adjust, will increase the stimulus, on the contrary, if significantly higher than expected, it will consider to further improve the quality of electric passenger car products; 3 the average fuel consumption and new energy vehicle points in parallel management policy reflects the government's intentions Radical, may also be adjusted appropriately; 4 future policy development will appropriately increase the inclination of leading enterprises.

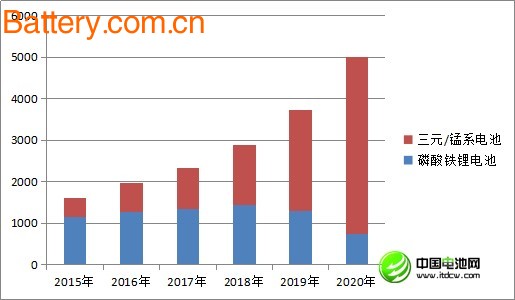

According to the forecast of new energy vehicle production and sales in Figure 8, true lithium research predicts that by 2020, the total demand for power lithium-ion batteries in China's new energy vehicle market will be close to 50 million kWh, of which lithium iron phosphate battery will also experience 2 years. Slow growth, absolute demand will decline by 2019, and rapidly drop to around 7.5 million kWh in 2020; it is expected that the ternary battery will be lifted in the field of pure electric buses in 2018, and the demand for ternary batteries will burst afterwards. 2020 will reach about 42.5 million kWh, thus basically completed the domination of the Chinese new energy automobile market, lithium iron phosphate batteries will be the market focus shifted to the storage area.

Figure 9. Demand forecast for power lithium-ion batteries in China's new energy vehicle market from 2016 to 2020 (unit: 10,000 kWh)

2, the conclusion

2.1 About the vehicle power battery

In order to popularize new energy vehicles, it is necessary to greatly increase the energy density of power batteries. How much is it better to improve? The "Energy Conservation and New Energy Vehicle Industry Development Plan (2012-2020)", which was led by the Ministry of Industry and Information Technology, clearly stated that the 2020 power battery module should have a specific energy of 300 Wh/kg. This means that the cell has an energy density of at least 350 Wh/kg. The goal of the Ministry of Science and Technology is relatively low. On April 26 this year, Minister Wan Gang publicly stated to the media that in the next five years, efforts should be made to double the energy density of the power battery to 300 Wh/kg, and the cost will be reduced by half to less than 1 yuan/Wh. (refers to the battery).

Based on this, True Lithium Research believes that the following two trends in the development of China's automotive power lithium-ion batteries in the next five years can be determined:

First, the lithium iron phosphate route will be phased out in the next three to four years. Under the large framework of the existing material system, no matter how the technology is improved, the lithium iron phosphate power battery cell has a higher energy density of 300 Wh/kg, and relatively speaking, the ternary/manganese lithium route hopes. There is great hope. What choices the country will make between the two is not difficult to judge. At present, the suspension of ternary batteries for electric buses is mainly due to safety considerations. Once the solution is found in terms of safety, the country will continue to support the ternary/lithium manganate power battery route. It is expected that in the two or three years starting this year, the state will intensively introduce a number of policy initiatives aimed at improving the safety of new energy vehicles. During this period, the problem of lithium iron phosphate is not big, but the practitioners who do not want to change the route need to take precautions and consider moving to the market such as energy storage after 2020.

Second, the industry consolidation process will accelerate. Although the ternary/lithium manganate route is more likely to reach 300Wh/kg, it will take a lot of hard work. Compared with big manufacturers such as BYD, CATL, Tianjin Lishen and Guoxuan Hi-Tech, it is more difficult for small and medium-sized manufacturers with significant gaps in manpower, material resources and financial resources to achieve this goal. In order to make the use of national financial funds and social resources more efficient, and make the input-output ratio of the industry more reasonable, the state may adopt measures to accelerate the elimination of a number of small and medium-sized manufacturers (such as raising technical thresholds, adjusting subsidy policies, etc.). In 2015, there were 120 manufacturers supplying power batteries to car companies, and it is expected to be controlled within 10 in 2020. More than 90% will be eliminated.

In summary, in the next few years, the focus of the development of China's automotive power lithium-ion battery will shift from “quantity†to “qualityâ€, and the best quality will win the world.

2.2 About the development of new energy vehicles

2016 is the first year of the third phase of China's new energy vehicle development (2016-2020). We believe that the third phase is generally the stage of rectification and upgrading. The purpose is to let China's new energy auto products finally go abroad and have international competitiveness. At the same time, the Chinese government has also set a target for industrial concentration. It is hoped that by 2020, only 2-3 companies will be left in the industrial chain of new energy vehicles, power batteries and even materials. It is not difficult to judge that the competent authorities will gradually introduce various measures to achieve these goals.

In addition, the target of 5 million new energy vehicles in 2020, the competent authorities must also complete. Therefore, in the next few years, the competent authorities will flexibly grasp the efforts of rectification and upgrading based on actual production and sales, and promote the steady and orderly development of China's new energy vehicle business.

SenKe Motorcycle

SenKe Motorcycle,SenKe Engine Spare Parts,SenKe Spare Parts,SenKe Raptor SK200

SONORA MOTOR COMPANY , https://www.sonoramotor.com